Farmland is the kind of asset people talk about as if it is a sure thing, until they need their money back quickly.

That gap between the story and the timeline is where most investor frustration starts. The truth is not complicated: farmland can be a strong long-term real asset, but it is not built for fast exits. If you accept that upfront, you can design a farmland plan that feels calm rather than forced.

This guide explains farmland liquidity in plain terms, including exit strategy options, the reality of secondary sales, and how to think about a holding period that fits your life.

What “Farmland Liquidity” Actually Means

Liquidity is simply how easily you can convert an investment into cash, at a fair price, when you need to.

With farmland, there are two different liquidity questions that often get mixed up:

- How liquid is the land itself?

- How liquid is the structure you invested in?

Global farmland practitioners make this distinction clear: the liquidity of the investment vehicle can differ from that of the underlying farms.

If you keep those separate, you make better decisions.

Why Farmland Is Illiquid (With Real Market Signals)

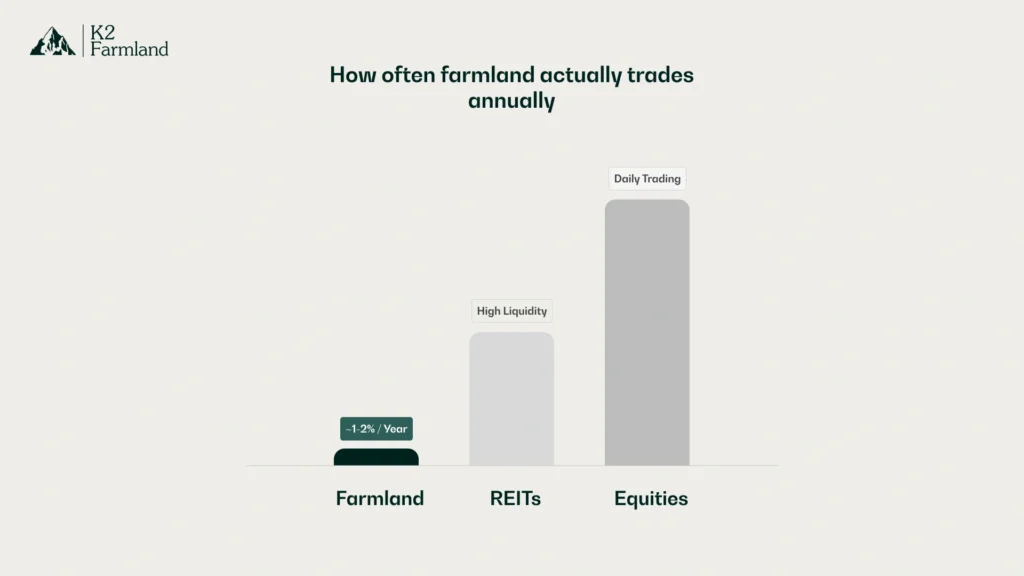

The most honest way to understand liquidity is to look at turnover.

Academic and industry research on farmland markets describes them as “thin,” meaning there are relatively few transactions each year. One research summary from the TIAA-CREF Center for Farmland Research notes evidence that annual transfer rates for arm’s-length production acreage are roughly 1-2 percent.

A separate Farm Foundation report similarly points out that in many row-crop regions, arm’s-length turnover runs around 1 percent per year.

When only about 1 to 2 percent of the market trades annually, liquidity behaves differently than equities or even urban real estate. In practical terms, it means:

- The buyer pool is narrower.

- Price discovery is slower.

- Exits can be seasonal and timing-sensitive.

This is not a flaw. It is simply how the asset class works.

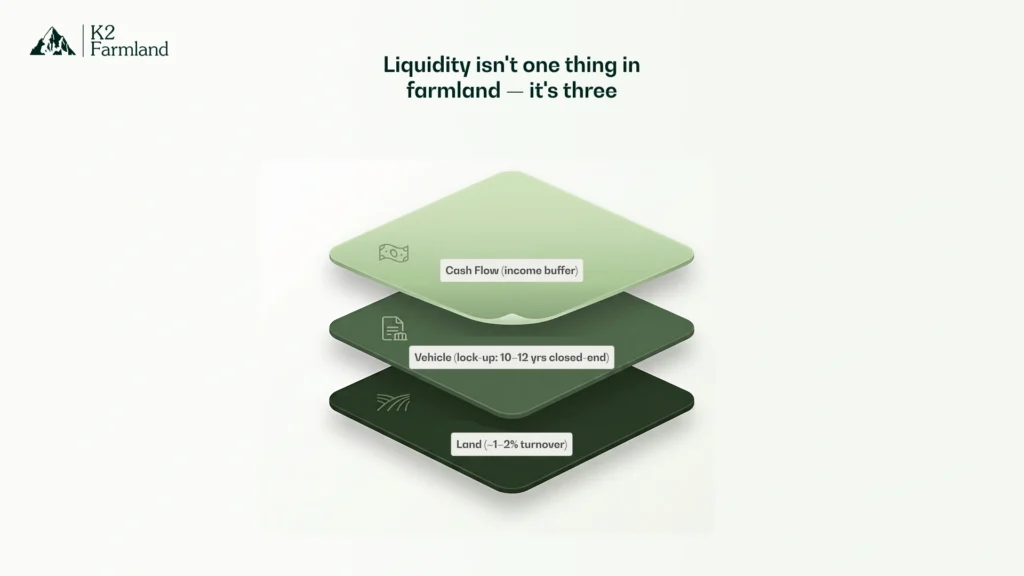

The Liquidity Stack: Land, Vehicle, And Cash Flow

A clean way to think about farmland liquidity is a three-layer stack.

Layer 1: Liquidity Of The Land

Direct farmland is typically sold through a private-market transaction. The same farmland market research notes higher transaction costs and longer holding periods as common features of real assets like farmland.

So, if your plan is “I will exit quickly if I change my mind,” direct land ownership is usually the wrong tool.

Layer 2: Liquidity Of The Vehicle

The structure you invest in can create more flexibility, but it also creates rules.

- Closed-end structures often lock capital for long periods until assets are sold. One evergreen-fund explainer contrasts this by noting closed-end funds often lock capital for around 10 to 12 years, while evergreen structures may allow redemptions based on terms.

- Evergreen vehicles may offer periodic liquidity windows, but they can be gated, delayed, or partially fulfilled under stress.

This matters because some investors buy “farmland” but are actually buying “a fund with a liquidity policy.”

Layer 3: Liquidity From Cash Flow

Cash flow is not the same as liquidity, but it reduces liquidity pressure.

If an asset produces steady net income, you are less likely to need an early sale. That is why many farmland strategies emphasize income-producing properties and measured operating improvements.

For context, the NCREIF Farmland Property Index is constructed from income-producing farmland properties, with returns tracked for income, appreciation, and total return. Properties are removed when they are sold, which highlights a basic truth: sale is the moment liquidity is realized.

Exit Strategy Options That Do Not Require “Selling The Story”

A practical exit strategy is not one path; it is a menu. Here are the most common exit routes, and what they really mean.

1. Primary Sale Of The Underlying Farm

This is the cleanest, most straightforward exit: sell the farm to a buyer.

A good primary sales plan usually includes:

- A clear buyer hypothesis (neighboring operators, regional aggregators, strategic buyers).

- Documentation readiness (title clarity, compliance, operating records).

- Operational improvements that are visible and transferable.

K2’s farm case study shows what a strategic sale can look like after operational transformation, describing a Year 5 sale to a strategic buyer and a reported 3.1x gross return on invested capital.

2. Staged Exits Instead Of Full Exits

Not every liquidity need requires a full sale.

Depending on the structure, staged exits can include:

- Partial sale of a stake in a holding entity.

- Recycling capital from mature assets while keeping exposure to the broader portfolio.

- Distributions from operating cash flow reduce the need to sell at an inconvenient time.

Whether this is possible depends entirely on legal structure and investor rights.

3. Vehicle-Level Liquidity Windows

If your priority is periodic liquidity, you may prefer structures designed for that, such as evergreen approaches with defined redemption mechanics.

The important part is the fine print: redemption frequency, notice periods, caps, and gating language.

If a manager cannot explain these clearly, treat that as a risk signal.

Secondary Sale: What It Is, And What It Is Not

A secondary sale is when investors sell their interest to another investor rather than the underlying asset.

The secondary market is where investors buy and sell securities among themselves, after issuance.

In farmland investing, “secondary sale” usually shows up in two ways:

Secondary Marketplace On Platforms

Some farmland investment platforms explicitly note lower liquidity because shares are not publicly traded, and they add that some platforms offer a secondary marketplace to help with disposition.

That can help, but it is not a guarantee of liquidity. Why:

- It depends on matching buyers and sellers.

- Pricing can be discounted when demand is low.

- Transfers may be subject to restrictions, fees, or timing limits.

Secondary Transfers In Private Deals

In private structures, secondary transfers may require:

- Manager consent, or right of first refusal.

- Legal re-papering.

- Buyer due diligence, because they are buying into an entity, not just a story.

If you want secondary-sale flexibility, it must be built into the structure from day one.

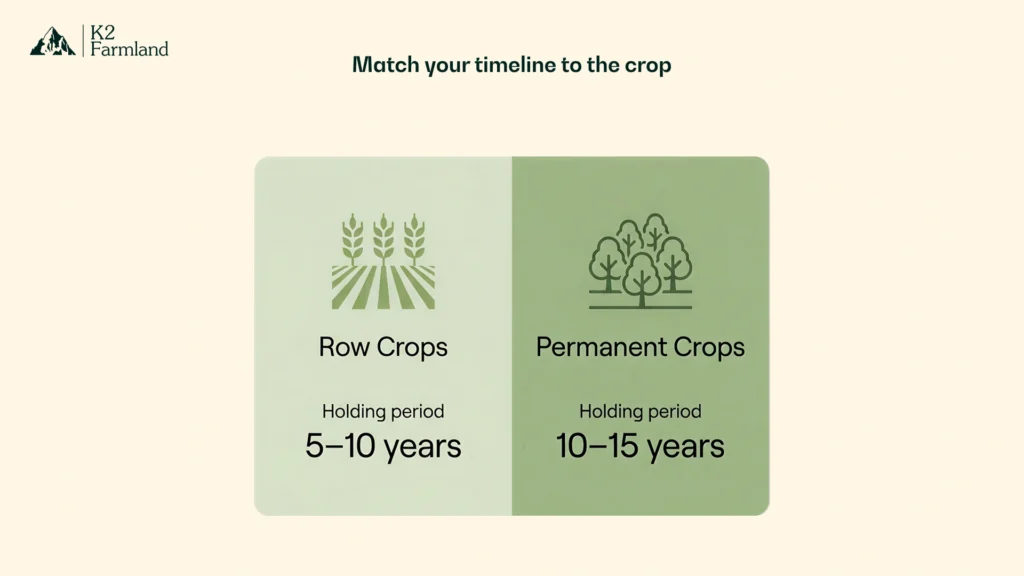

How To Choose A Holding Period That Matches Real Life

Most liquidity mistakes happen because the investor never chose a real holding period.

A farmland investing guide gives a practical benchmark: row crop investments often target about 5 to 10 years, and permanent crops can be closer to 10 to 15 years, given time-to-maturity dynamics.

You do not have to copy those numbers exactly, but they show the mindset: farmland is usually a multi-year decision.

A simple way to set your holding period:

- List your known cash needs in the next 3, 5, and 10 years.

- Only allocate “patient capital” to farmland.

- Keep a separate liquidity buffer outside the farmland allocation.

- Choose a structure whose redemption and exit mechanics match your timeline.

A Practical Liquidity Checklist Before You Invest

Use this checklist to avoid buying a narrative only to discover the lock-up later.

Structure And Rights

- What is the expected holding period, and what events trigger a sale?

- Are there redemption windows, and can they be gated or delayed?

- Can you do a secondary sale, and what approvals are needed?

Sale Readiness

- Is the asset income-producing and documented as such?

- Are operating records and compliance clean enough for a buyer to underwrite quickly?

- Is there a clear buyer set, or will it depend on “someone will want it”?

Personal Fit

- If you needed cash earlier than planned, do you have options outside this investment?

- Would a delayed exit harm your finances, or simply annoy you?

If it would harm you, you are overweight, or in the wrong structure.

How K2 Approaches Liquidity And Value Realization

K2’s positioning is operator-led, meaning value is created through operations, diversification, and measurable stewardship, rather than speculation on price alone.

From a liquidity perspective, this matters because:

- Stronger, more diversified cash flows can reduce the need for forced exits.

- A documented operational track record can make a strategic sale easier to execute at the right time.

- The firm explicitly describes structured ownership for compliance and investor security, which requires clearly defined exit rights.

FAQs

Is Farmland Liquidity Better In A Fund Or Direct Ownership?

Often, the vehicle can provide more planned liquidity than direct land, but it depends on redemption terms and whether withdrawals can be gated.

What Does “Secondary Sale” Mean In Farmland Investing?

It usually means selling your interest to another investor instead of selling the farm itself, similar to how secondary markets work for other securities.

What Is A Reasonable Holding Period For Farmland?

Holding periods vary, but one practical benchmark suggests 5 to 10 years for row crops and 10 to 15 years for permanent crops, reflecting maturity and value realization timelines.

Why Do People Say Farmland Markets Are “Thin”?

Because relatively few farmland trades occur each year. Research highlights low annual turnover and transfer rates, roughly in the 1 to 2 percent range, in production markets.

Can An Operator Improve Liquidity?

An operator cannot change market turnover, but strong operations can improve sales readiness, buyer confidence, and the odds of a strategic exit when you choose to sell.

Conclusion

Thinking clearly about farmland liquidity does not reduce the asset’s value. It protects you from buying the wrong structure, at the wrong time, for the wrong reasons.

Key takeaways:

- Farmland is typically illiquid because markets are thin and turnover is low, often cited at around 1 to 2 percent annually in production markets.

- Liquidity depends on three layers: the land, the investment vehicle, and the asset’s cash flow.

- Secondary sale can exist, but it does not guarantee liquidity and must be designed into the structure.

- A realistic holding-period mindset matters, with benchmarks often discussed in multi-year ranges, such as 5 to 10 years for row crops and longer for permanent crops.

- The best liquidity plan is boring and effective: match structure to timeline, keep a cash buffer, and avoid forced exits.